China is hardly the first country to attempt to purchase oil in yuan rather than dollars, and it appears to have found a willing seller. Saudi Arabia, which sends 25% of its total output to China, is considering making these sales in yuan, according to the Wall Street Journal.

These negotiations, which have risen and fallen in intensity over the last half-decade, are unlikely to conclude anytime soon. For one thing, Saudi Arabia links its riyal to the dollar, which means that any damage done to the dollar inadvertently will hurt the riyal. However, because the US’ geopolitical power is so dependent on the petrodollar — with 80 percent of global oil transactions priced in dollars — the issue is perpetually present. What would the world be like if the petroyuan became the preferred currency of the oil industry?

The US economic hegemony was established on the back of the petrodollar. The dollar’s healthy status as a reserve currency is largely due to the US economy’s strength. However, it also stems from the dollar’s abundant liquidity, which is partly the outcome of governments retaining pools of dollar reserves for the purpose of purchasing oil.

This connection was established in the early 1970s, shortly after President Richard Nixon disconnected the dollar from gold. In 1974, Washington and Riyadh reached an agreement under which Saudi Arabia could purchase US Treasury bills prior to their auction. Saudi Arabia would then sell its oil in dollars, so increasing the currency’s liquidity and allowing those dollars to be used to purchase US debt and products. David Spiro, a political economist, outlined how Saudi Arabia influenced other OPEC members to invoice oil in dollars rather than a basket of other currencies in his book The Hidden Hand of American Hegemony.

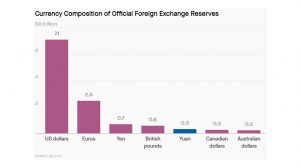

If the yuan displaces the dollar sufficiently in the annual $14 trillion global oil trade — which is impossible to quantify — governments will be forced to retain yuan reserves instead. (At the moment, 2.48 percent of global reserves are in yuan, compared to 55% in dollars, according to IMF data.) Oil producers receiving yuan would be required to spend money on Chinese debt and imports, further bolstering China’s economy; however, if the globe is unusually flush with yuan, other transactions, such as metals or soybeans, may begin to be conducted in yuan.

The repercussions would be serious for both China and the US. To maintain the yuan’s new role, China must offer political stability and financial transparency on a par with what the US pledged in the twentieth century. The US’s ability to issue dollar debt and earn dollars through exports would deteriorate, resulting in the contraction of its economy. In this scenario, a declining dollar may set off a vicious cycle of capital flight away from the dollar and toward the yuan, further weakening the dollar.

Experts believe that these occurrences are improbable. However, examining these dependencies serves as a valuable reminder of how much of our contemporary moment—from the success of sanctions to the advancement of green energy—is contingent on the strength of the US dollar.

Also Read: Six Strategies from Donald Trump’s PR playbook